Financial Maths

Formulae from Maths Tables

Video Examples and Questions with Solutions

Videos explaining the examples from T&T6 Chapter 5

13 videos (29:55)

Videos explaining the examples from T&T6 Chapter 5

13 videos (29:55)

|

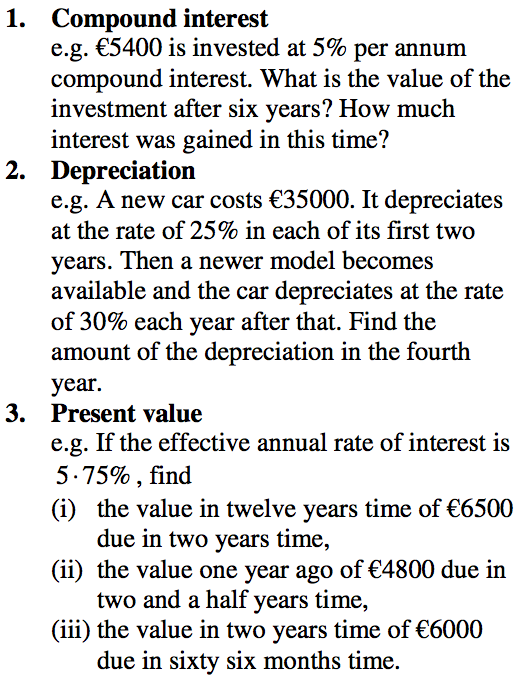

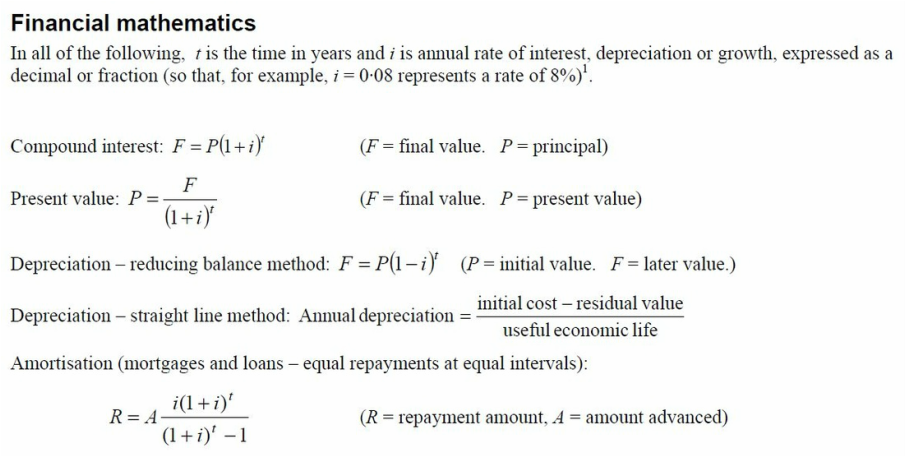

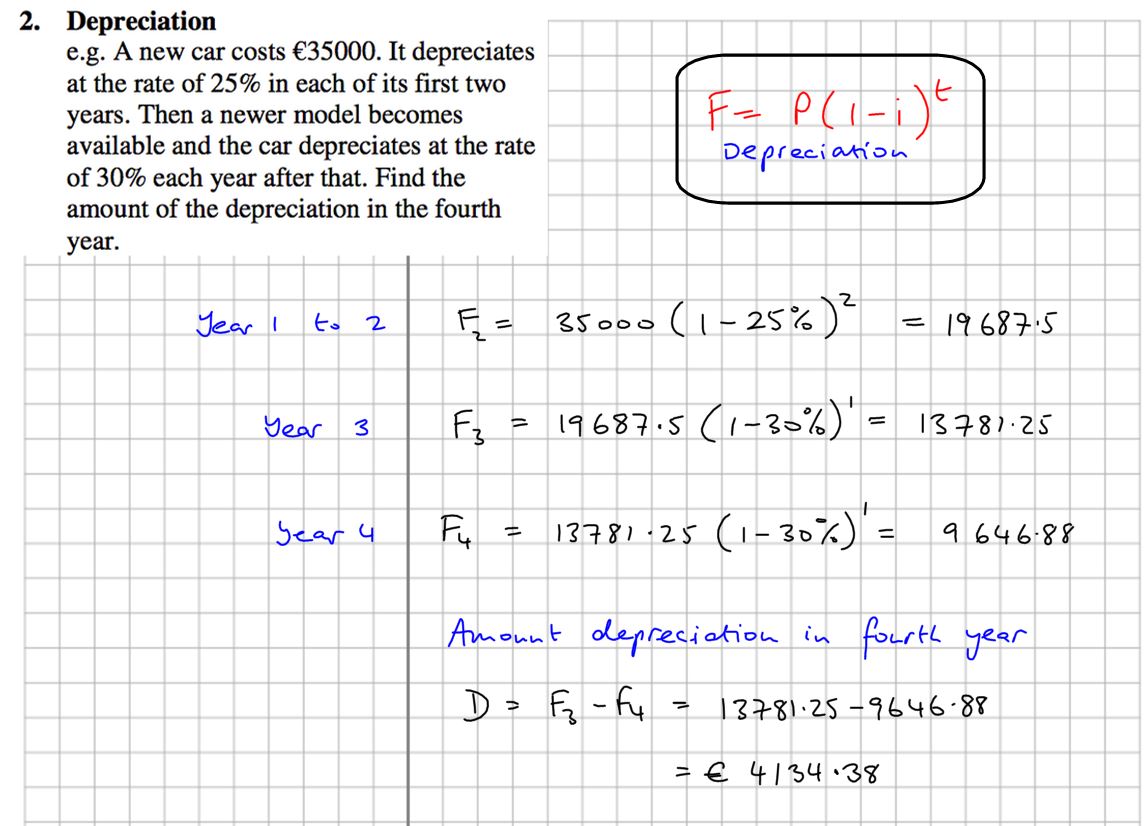

Section 5.1 Compound Interest

5 videos (9:51) |

|

|

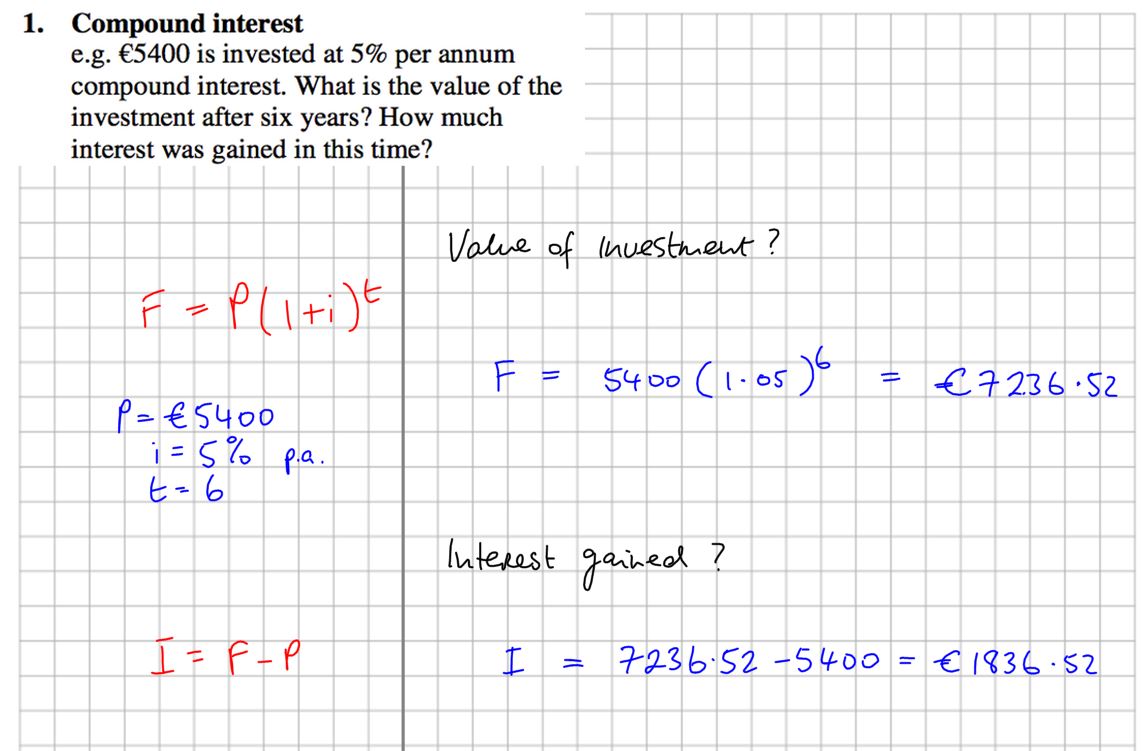

Section 5.2 Depreciation

2 videos (2:50) |

|

|

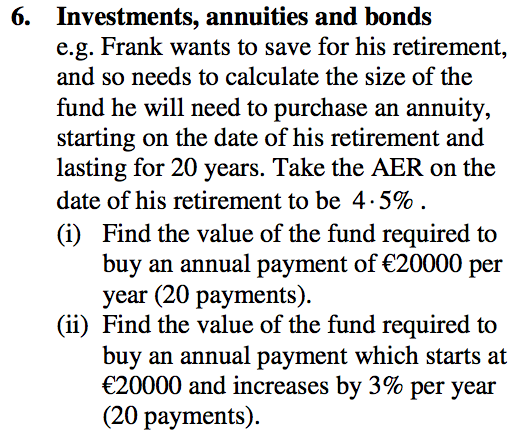

Section 5.3 Annuities and Pensions

4 Videos (13:15) |

|

|

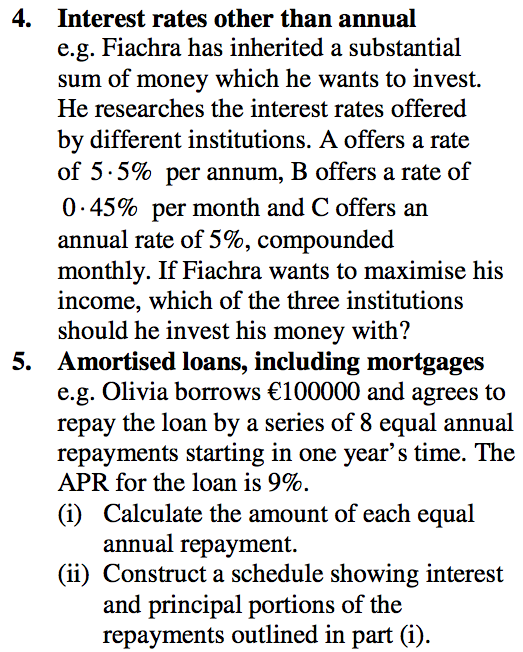

Section 5.4 Loans and Mortgages

2 Videos (3:59) |

|

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}